[Quant] Alpha#101

업데이트:

Wilmott Magazine 2016(84) (2016) 72-80 [Paper]

Zura Kakushadze

In this post, we examine Alpha #101 from the paper’s collection of 101 formulaic alphas.

Formula

\[\frac{\text{close} - \text{open}}{(\text{high} - \text{low}) + 0.01}\]- close − open : How much did the price rise (or fall) during the day?

- high − low : How much did the price fluctuate during the day?

- + 0.01 : A small constant to prevent division by zero.

In essence, this alpha measures the efficiency of the move relative to volatility.

High alpha value →

- The price rose quietly, with little fluctuation.

- A steady, confident upward move — possibly conviction-driven buying.

Low alpha value →

- High intraday volatility relative to the net move.

- An unstable, noisy price action.

This alpha can serve as a useful signal for short-term trading or momentum screening.

Limitations

- The signal only looks at a single day’s OHLC data.

- It ignores all other information (volume, news, macro, etc.) and should be combined with other indicators.

- In a regime of high market-wide volatility, the interpretation may change significantly.

Experiment

Setup

| Parameter | Value |

|---|---|

| Universe | Top 30 stocks from the S&P 500 |

| Starting Capital | $1 |

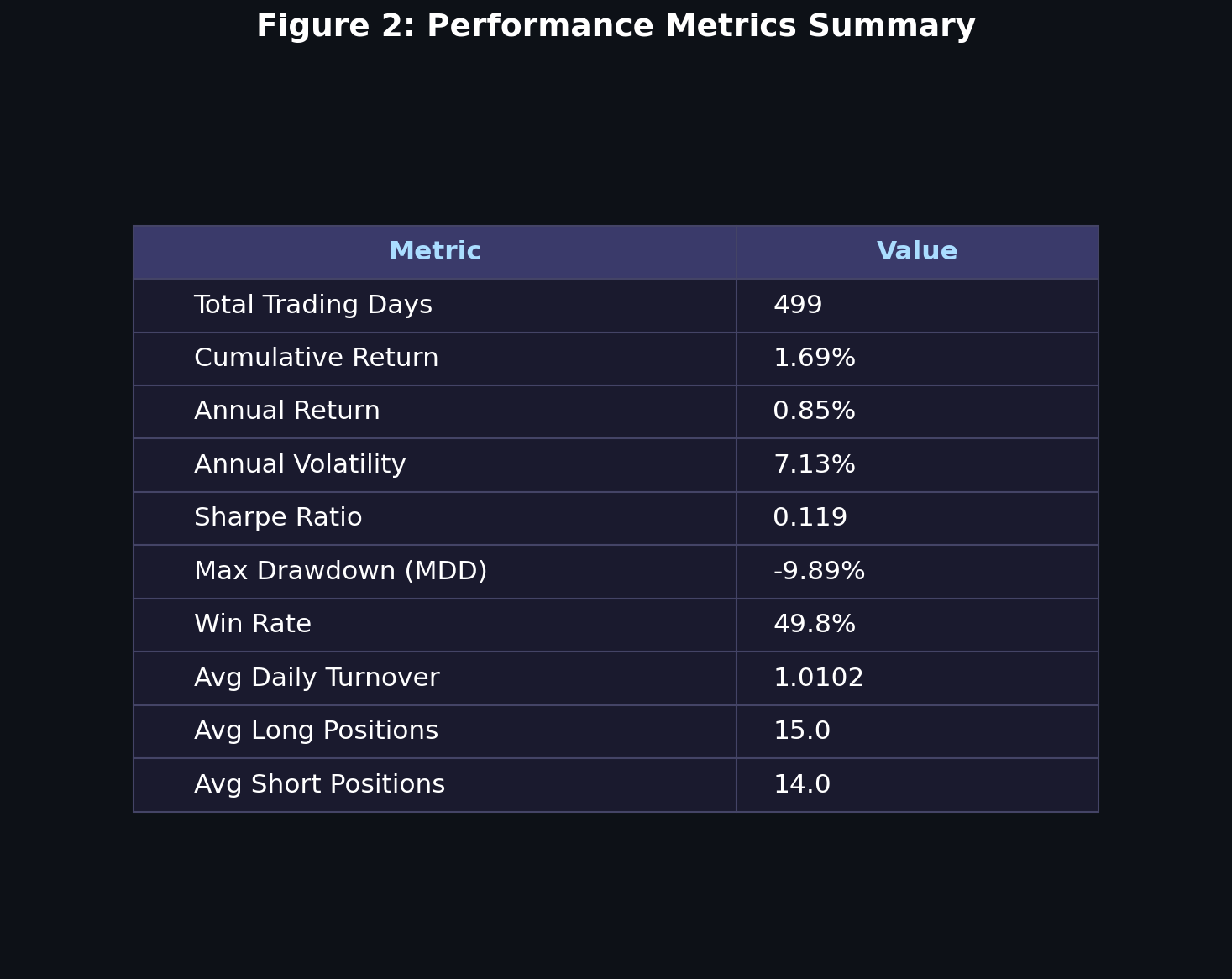

| Period | 499 trading days (~2 years) |

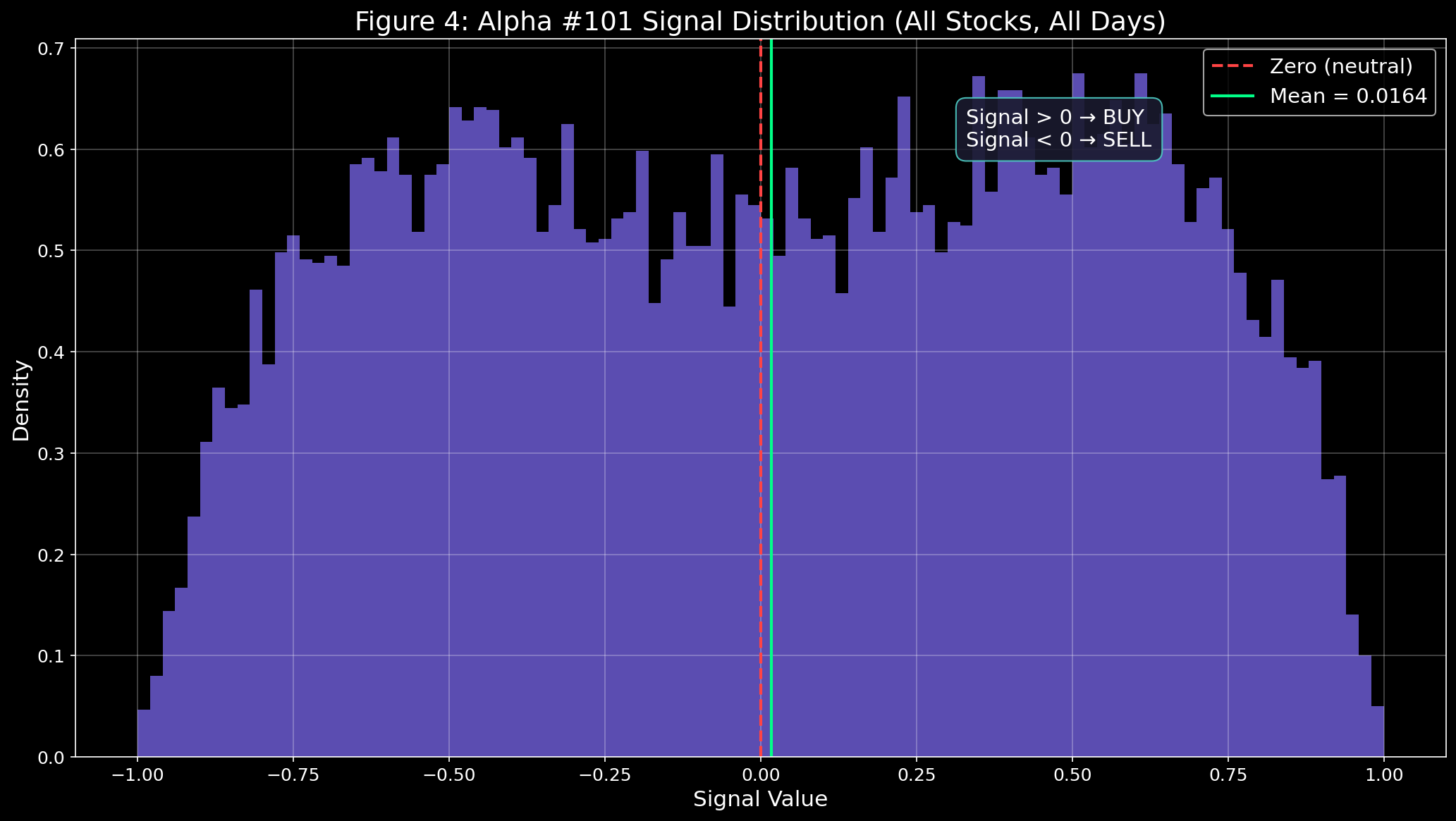

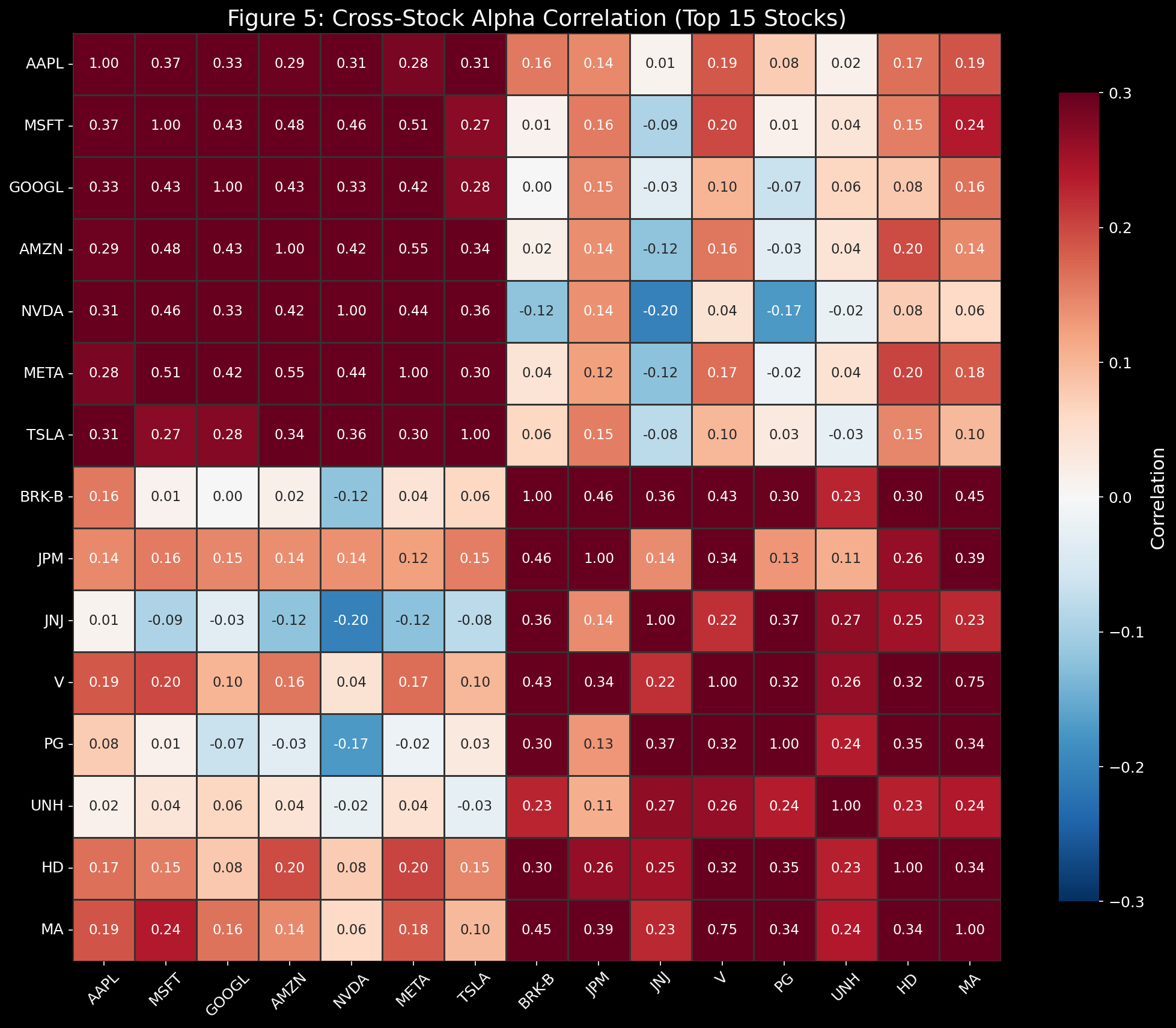

Applying the signal to 30 stocks over ~500 days produces a total of 15,000 alpha signals.

Procedure

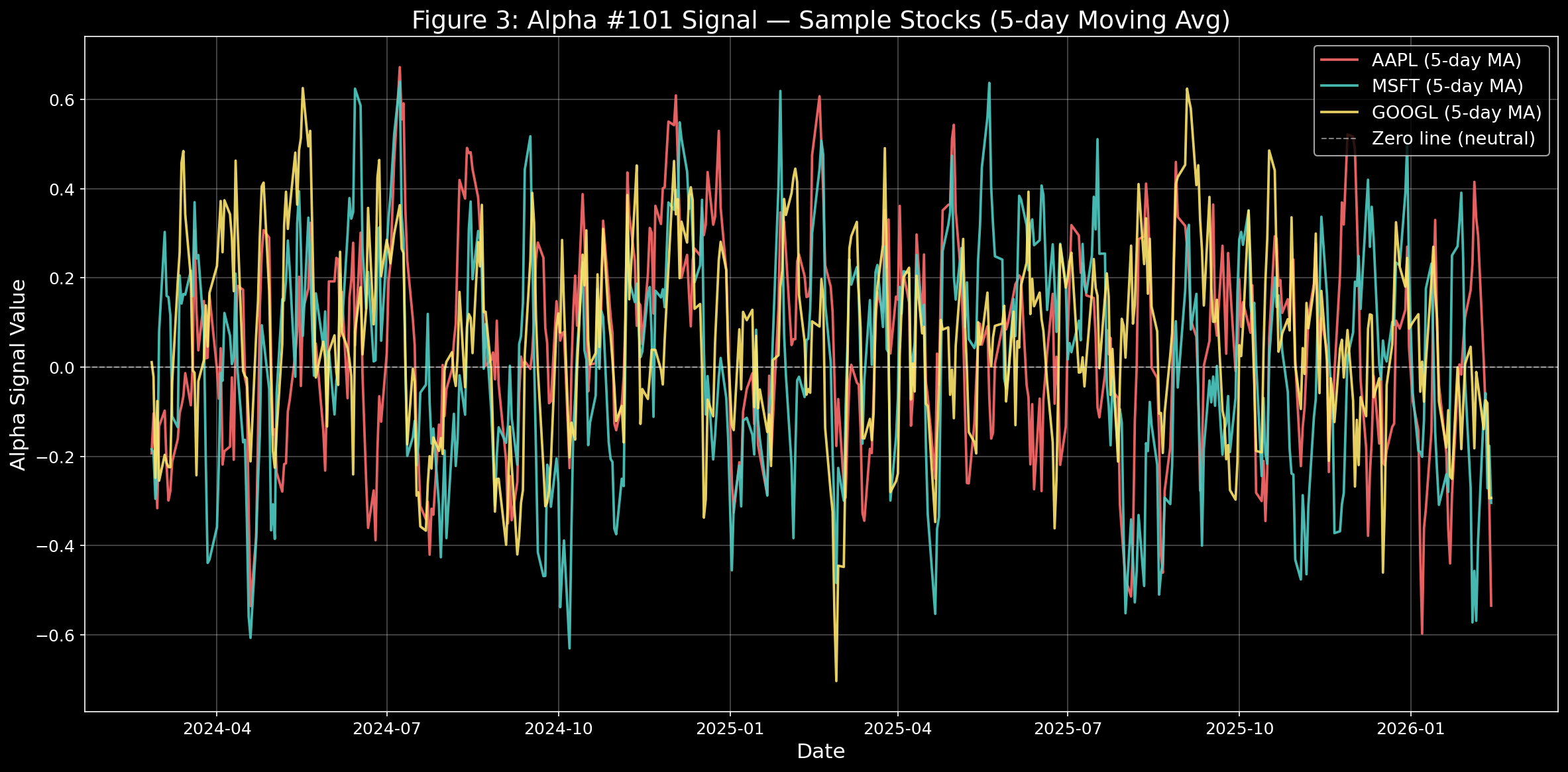

- Compute the alpha signal for each stock and rank them cross-sectionally.

- Since close, high, and low prices are only available after market close, the ranking is applied with a one-day lag.

- Go long the top 50% and short the bottom 50% by rank.

- Calculate the daily portfolio return across all stocks.

- Compound the daily returns to get the cumulative PnL.

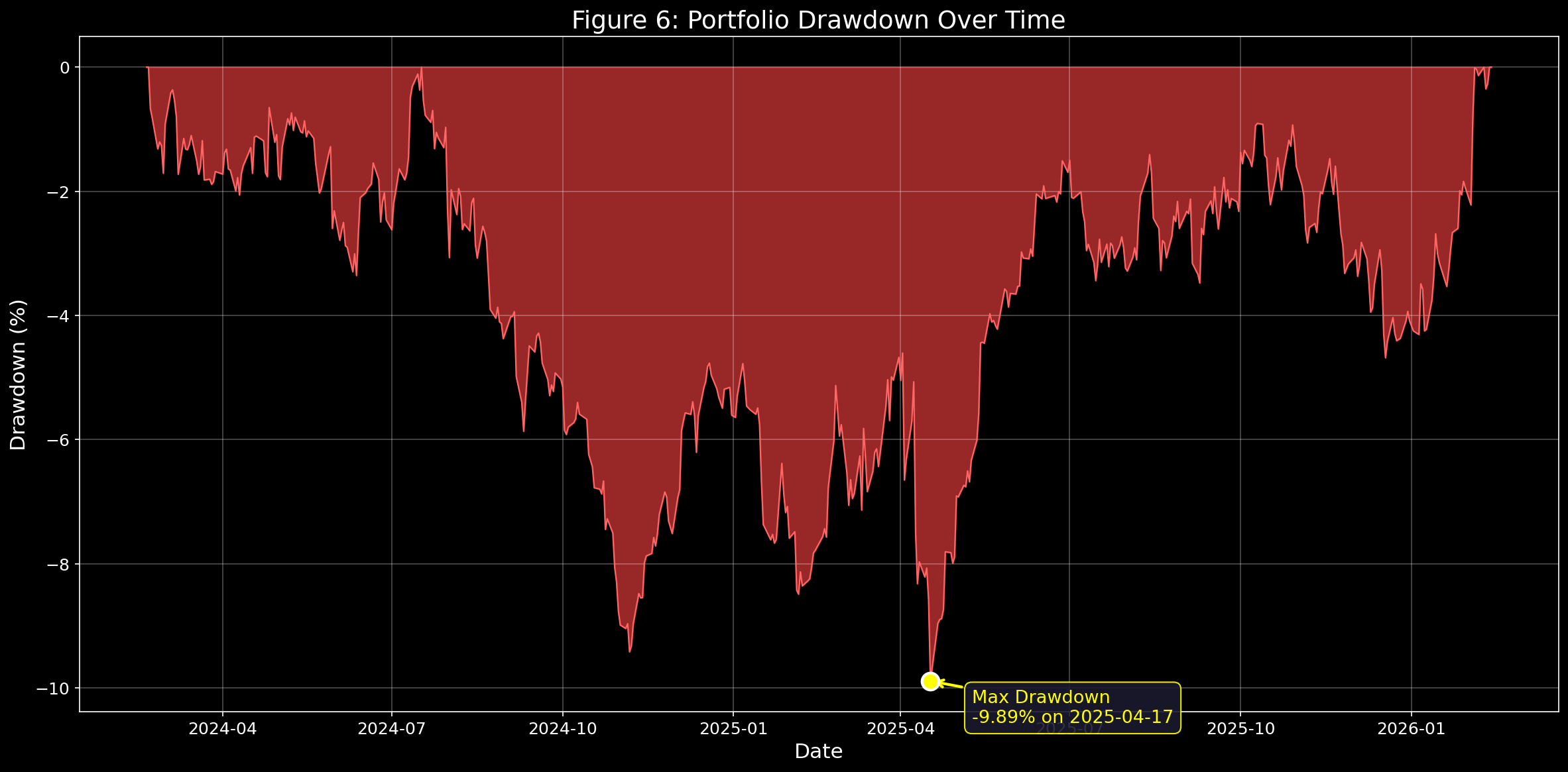

Results

- The starting point of $1 is the break-even line.

- PnL = Profit and Loss

Key Metrics

- Total Return: 1.69% — Quite low, considering bank deposit rates sit around 2–3% annually.

- Annual Volatility — How much the portfolio value fluctuated over the year.

Why Do We Multiply by √N?

This is a fundamental rule in statistics:

\[\sigma_{N\text{-day}} = \sigma_{1\text{-day}} \times \sqrt{N}\]Why not just multiply by N?

Daily volatility: 1%

If we simply multiplied:

→ 252-day volatility = 1% × 252 = 252% (absurd!)

With the square root:

→ 252-day volatility = 1% × √252 = 1% × 15.87 = 15.87% (realistic)

The underlying principle:

Daily returns are assumed to be independent. Today’s +1% doesn’t dictate tomorrow’s direction — gains and losses can cancel out over time.

Mathematically:

\[\text{Var}_{N} = N \cdot \sigma^2 \quad \Rightarrow \quad \text{Std}_{N} = \sqrt{N} \cdot \sigma\]Variance scales linearly with $N$; standard deviation scales with $\sqrt{N}$.

Annual Volatility Benchmarks

| Asset | Annual Volatility | Note |

|---|---|---|

| S&P 500 | 15–18% | U.S. large-cap 500 |

| NASDAQ | 20–25% | Tech-heavy, higher swings |

| KOSPI | 18–22% | Korean equity market |

| Bitcoin | 80–120% | Extreme volatility |

| U.S. Treasuries | 3–5% | Very stable |

| Our Strategy | 7.13% | Remarkably low volatility |

Other Metrics

- Sharpe Ratio — Risk-adjusted return:

A Sharpe above 1.0 is considered good; above 2.0 is excellent. Our result of 0.119 is very poor.

- Max Drawdown — The largest peak-to-trough decline in portfolio value.

- Win Rate — Percentage of trading days with a positive return.

- Avg Daily Turnover — How much of the portfolio is reshuffled each day.

- A value of 1.01 means we traded ~101% of the portfolio’s value daily. Higher turnover = higher transaction costs.

- Avg Long / Short Positions — The average number of stocks held long vs. sold short on any given day.

Disclaimer: This post is purely a study note. All investment decisions should be made based on your own research and judgment.

댓글남기기